The Parent Files, Part 2: The Debt That Doesn’t Die

Still Paying for Someone Who Erased You

The Hook That Stops Your Heart

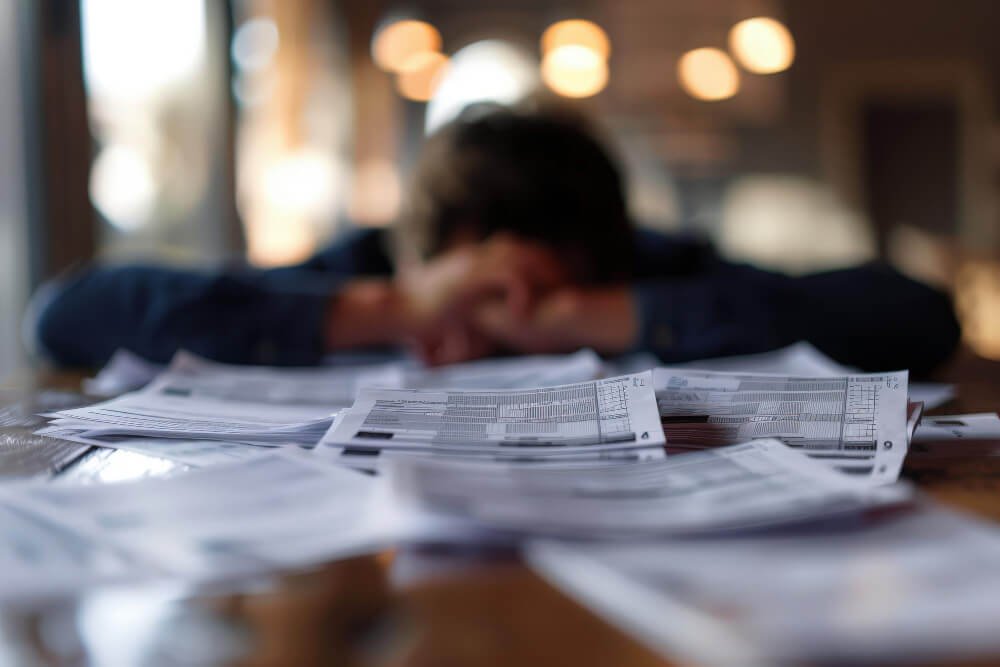

The email arrives at 6:47 AM. Subject line: “Payment Processed – Parent PLUS Loan.”

Amount: $1,247.83

Remaining balance: $67,439.22

Estimated payoff date: November 2037

Your daughter blocked your number fourteen months ago. Changed her last name on social media. Told the extended family you’re dead. But Navient doesn’t care about estrangement. The Department of Education doesn’t pause for broken hearts. Every month on the 15th, the money leaves your account for someone who won’t acknowledge you exist.

You’re 68 years old. You’ll be 80 when it’s paid off. If you live that long.

The bitter math: you might die before the debt does. And even then, it might follow you. Parent PLUS loans can pursue your estate, drain your life insurance, take the house you thought you’d leave to… well, you used to know who.

The Financial Truth No One Will Say

Let’s talk about what estrangement actually costs. Not emotionally—that price is infinite. Let’s talk dollars. The numbers that don’t care about your feelings. The mathematics of loving someone who’s made you a stranger.

The Monthly Hemorrhage

Here’s what leaves your account every month for your estranged child:

- Parent PLUS loan payment: $1,247.83

- Their phone (still on your plan): $47.99

- Car insurance (they don’t know you pay): $189.00

- Health insurance (through your work): $412.00

- Netflix/Spotify family plan: $31.98

- Storage unit with their things: $127.00

- Life insurance naming them beneficiary: $89.00

Monthly total: $2,144.80

Annual total: $25,737.60

Decade total: $257,376.00

You’ll work until you die. Not because you want to. Because someone you haven’t spoken to in years still costs two thousand dollars a month.

The Parent PLUS Apocalypse

Parent PLUS loans are the predator nobody warns you about. They’re federal loans, which sounds safe. Official. Regulated. What they are is financial quicksand designed to drown parents who love too much.

The trap you walked into:

- No borrowing limits based on ability to pay

- Interest rates higher than student federal loans (currently 8.05%)

- Your retirement income can be garnished

- Your Social Security can be taken

- No statute of limitations

- Death might not discharge them (depends on the loan)

You borrowed $85,000 over four years. You’ve paid $43,000 so far. You still owe $67,439. The math doesn’t math because interest is a vampire that feeds while you sleep.

Your financial advisor—the one you finally saw at 67 when the panic set in—did the calculation. At your current payment rate, you’ll pay $149,739 total for that $85,000 education. The education that taught your child you’re toxic.

Reflection Check-In #1

What financial sacrifice hurts the most right now?

⬜ A) The retirement that disappeared

Consider one small thing you can do today for your future self – even opening a $25 savings account can be an act of self-recognition

⬜ B) The house I’ll have to sell

Before any big decisions, document what this house has meant. Take photos. Write the memories. The house held love – that doesn’t leave with a sale

⬜ C) The bankruptcy I’m considering

Bankruptcy isn’t moral failure – it’s a legal tool. Consider a consultation with a nonprofit credit counselor first. You deserve informed choices

⬜ D) The credit cards maxed for their life

Call one card company today and ask about hardship programs. Many have unpublished options. One small step toward breathing room

⬜ E) Working past 70 with failing health

Your body has carried so much. What’s one kind thing you can do for it today? Even a five-minute walk or extra glass of water honors what you’ve endured

⬜ F) The inheritance that became debt

Write a letter to your younger self about what you hoped to leave behind. The love you intended to pass on still exists, even if the money doesn’t

⬜ G) Other

Whatever specific pain you’re carrying deserves to be named. Write it down. Sometimes seeing it on paper makes it smaller than it feels in your chest

The Secret Payments They’ll Never Know

Beyond the Parent PLUS disaster, there’s the hidden financial architecture of estrangement. The bills you pay that they don’t know about. The financial protection you maintain despite their rejection.

Health Insurance: The Silent $412

They aged off your insurance at 26, got a job with “benefits.” Those benefits have a $6,000 deductible. When they posted about needing emergency surgery last year, you called HR. Added them back during open enrollment. Claimed they were “financially dependent” on you. A lie that’s also the truth.

They don’t know. The insurance card goes to your address. You forward it in an envelope with no return address. Their Instagram story from the ER thanked “universal healthcare advocates” for inspiring them. The universe, apparently, is you paying $412 a month.

The Phone Bill Archaeology

Their number is still on your family plan. $47.99 a month to maintain a line that will never call you. But you can see the data usage. Proof of life. 47GB last month. They’re alive. They’re scrolling. They’re talking to everyone but you.

You could cut it off. Force the issue. But what if there’s an emergency? What if they need to call 911? What if, what if, what if. So, you pay. Every month. For the possibility of a call that never comes.

The Car Insurance Ghost Policy

The car is in their name now. You signed it over at graduation. But you know they’re driving uninsured—saw the registration sticker expired in a photo they posted. So, you added them to your policy. Listed the car as “garaged at your address.” Another lie that keeps them safe.

$189 a month. They’ll never file a claim through you. But if they hit someone, if someone hits them, there’s coverage. Protection they don’t want from a parent they’ve erased.

The Retirement That Became Tuition

You had $340,000 in your 401k at age 55. Good, not great, but enough. Then came the college years. The “dream school” acceptance. The out-of-state tuition. The conviction that education was the gift that couldn’t be taken away.

The withdrawals:

- Freshman year: $42,000

- Sophomore year: $38,000 (you learned to be “smarter”)

- Junior year: $44,000 (studied abroad, “once in a lifetime”)

- Senior year: $47,000 (thesis year, couldn’t work part-time)

Total withdrawn: $171,000

But that’s not the real cost. That $171,000, if left alone, would have been $487,000 by now. Would have been $743,000 by retirement. Would have been security, dignity, choice.

Instead, you have $73,000 left. At 68. Your financial advisor stops suggesting retirement. Now she talks about “work-life integration” and “encore careers.” Corporate speak for “you’ll die at your desk.”

The Second Mortgage Nobody Mentions

The house was supposed to be paid off by now. Would have been, except for the second mortgage. $75,000 borrowed against the equity. For what? Their rehab that didn’t take. Their wedding you weren’t invited to. Their grad school they didn’t finish. Their startup that never started.

Now you pay $1,100 for the first mortgage, $630 for the second. The house worth $400,000 carries $185,000 in debt. The equity you built over 30 years became their spending money. The inheritance they would have received became debt they’ll never know about.

Your sister asks why you don’t downsize. Move to a condo. Something “more manageable.” You can’t tell her the house is underwater with love. That selling means admitting they’re never coming home.

Reflection Check-In #2

If you could eliminate one financial burden today, which would free you most?

⬜ A) The Parent PLUS loan payments

Research Income-Driven Repayment plans today. Some parents don’t know these exist for PLUS loans. The application takes 10 minutes online

⬜ B) The second mortgage

Contact a HUD-approved housing counselor (free service). They know options banks don’t advertise. You might have more choices than you think

⬜ C) The credit card debt from their life

Try the avalanche or snowball method – even $5 extra toward principal this month is movement. Forward motion matters more than speed

⬜ D) The ongoing monthly bills for them

Choose one small bill to release this month. Maybe start with Netflix. Practice letting go in small doses before the big decisions

⬜ E) The emotional spending to fill the void

When the urge to spend hits, write what you’re really trying to buy. Connection? Proof of love? Name it first, then decide

⬜ F) The therapy to understand why

Look into OpenPath Collective or Better Help’s financial aid. Therapy at $30-60/session exists. Understanding doesn’t have to be unaffordable

⬜ G) Other:

Your specific burden is valid. Consider telling one trusted person about it today. Secrets gain weight in silence

Bankruptcy at 67: The New American Retirement

You’ve said the word out loud now. Bankruptcy. Your generation doesn’t do bankruptcy. Your generation pays their debts, keeps their word, maintains their credit. But your generation didn’t anticipate this.

The lawyer—$300 consultation you paid with a credit card—explained your options:

Chapter 7: Liquidation. Lose the house, keep the debt (Parent PLUS loans rarely discharge).

Chapter 13: Reorganization. Payment plan for 3-5 years, might keep the house.

Neither option touches the Parent PLUS loans. Those are “yours until death.” The lawyer actually said that. Yours until death. Like a prison sentence for loving too much.

The paralegal, young enough to be your granddaughter, asked, “Why did you borrow so much for your child’s education?”

How do you explain that in 2010, everyone said education was everything? That student loans were “good debt”? That you were investing in their future. How do you explain that love doesn’t read fine print?

The Credit Card Archaeology

The statements tell a story. Not your story—theirs. Traced through plastic:

Chase Sapphire: $14,847 balance

- Spring break 2018 (they were “too stressed” to not go)

- Textbooks every semester (why were books not included?)

- Therapy co-pays (the therapy that diagnosed you as toxic)

- Moving expenses to the city they didn’t tell you about

Bank of America: $11,232 balance

- The apartment deposits you co-signed

- The car repairs for the car you bought them

- The medical bills from when they were uninsured

- Plane tickets home they didn’t use

Discover: $8,743 balance

- Groceries during their unemployment

- Phone bills before you added them back

- The graduation dinner they didn’t attend

- Christmas presents returned to sender

Total credit card debt: $34,822 Minimum payments: $1,047/month Interest charges: $587/month

You’re paying $587 a month in interest for memories they’re trying to forget.

The Money You Send Anyway

The Venmo requests come randomly. Always urgent. Always without context. Just amounts:

- $400

- $1,200

- $87

- $2,400

No explanation. No thank you. No acknowledgment of what this costs you. But you send it. Every time. The memo line says “DO NOT CONTACT” now. You respect that. Love with a muzzle. Care with conditions. Financial support with silence attached.

Your bank flags it as unusual activity. “Did you authorize this payment?” Yes. “Do you know this person?” Not anymore.

Last month’s request was $3,400. Probably rent and deposit on a new place. You sent it from the home equity line of credit. Adding debt to debt. Building a monument to absence.

Reflection Check-In #3

What do you tell yourself when you send money into silence?

⬜ A) They must really need it

Your care is real even if their need is unclear. Consider setting a monthly limit you can live with – boundaries can coexist with love

⬜ B) At least they’re reaching out somehow

This counts as contact, even if it’s not the kind you want. Maybe keep a log of these moments – they’re proof the connection isn’t completely severed

⬜ C) This maintains some connection

It does, and that’s okay to need. Consider if you can maintain connection in ways that don’t hurt you financially

⬜ D) It’s what parents do

Parents also deserve security and peace. Write down what your parents did for you – was it everything? You’re allowed to be human too

⬜ E) Maybe this time they’ll say thank you

Hope is painful when it’s always deferred. What if you thanked yourself each time instead? You’re the one who deserves acknowledgment

⬜ F) I can’t let them struggle even if they hate me

Love doesn’t require your destruction. Consider: would they want you to suffer this much? If not, honor that. If yes, what does that tell you?

⬜ G) Other:

Your reason is yours and it’s valid. But also ask: would you accept this reasoning from a friend in your situation?

Working Until Death: The New Reality

You were supposed to retire at 65. Travel. Garden. Whatever people do when they stop being ATMs for estranged children. Instead, you’re 68 and requesting more hours. Taking consulting gigs. Driving Uber on weekends with a car that has 200,000 miles.

Your body keeps score:

- The knees that need replacement (can’t afford the time off)

- The blood pressure medication (stress is expensive)

- The therapy you stopped (choosing loan payments instead)

- The dental work delayed (maybe next year)

- The colonoscopy postponed (who has time?)

Your manager, fifteen years younger, talks about “succession planning.” They want to train your replacement. You nod, smile, say you’re “thinking about it.” You’re thinking you’ll die at this desk. The life insurance will pay off the Parent PLUS loan. Finally, freedom through death.

The Relatives Who Don’t Understand

“Just stop paying for things,” your brother says. He has three kids who call weekly. His loans are paid off. His retirement is funded. His world makes sense.

“Let them face consequences,” your sister suggests. Her daughter brought grandkids for Thanksgiving. Her son-in-law fixed her porch. Her love has returns.

They don’t understand that consequences require contact. That boundaries need someone on the other side to recognize them. That you can’t teach lessons to ghosts.

They don’t understand that the money isn’t the connection—it’s the only proof you existed in their life. The only evidence you still care. The only way to say “I love you” that doesn’t get returned to sender.

The Will That Keeps Changing

You’ve rewritten it four times this year. They’re in. They’re out. They’re in but with conditions. They’re out but with explanations.

Current version: They get everything. No conditions. No requirements to attend the funeral. No forced reconciliation. Just the house they’ll sell, the life insurance that will finally clear the debts, the possessions they’ll probably donate without looking through.

The lawyer asks, “Are you sure?” You’re not sure of anything anymore. But dying with conditions feels like extending the estrangement into eternity. So yes, they get everything. Even your death will be a gift they don’t acknowledge.

The Financial Advisor Who Sees Everything

Maria has been your advisor for three years now. She’s seen the numbers. Run the projections. Done the math that says you’ll never retire. She knows about the estrangement—hard to explain why you’re broke at 68 with a good career without mentioning the child-shaped hole in your finances.

“Have you considered…” she starts, then stops. Considered what? Not paying? Letting them suffer? Choosing myself? Yes. Every day. Then the 15th comes and the payment processes and the consideration becomes continuation.

She shows you charts. If you stopped all payments to your child, you could retire in 18 months. If you sold the house, paid off debts, moved to a studio apartment, you could stop working. If you chose yourself, you could rest.

The charts assume choice is possible. They don’t factor in love’s inability to do math.

Reflection Check-In #4

What would you do with the money if you stopped paying for them?

⬜ A) Finally retire and rest

Calculate exactly what date you could retire if you stopped payments today. Write it on a calendar. Let yourself imagine that day, even if you don’t choose it

⬜ B) Get the medical procedures I’ve delayed

Make one medical appointment this week, even if just for a checkup. Your body has been waiting patiently. It deserves attention

⬜ C) Travel to places I dreamed about

Create a Pinterest board or folder of these places. Dreams don’t cost anything to keep alive. Start with free planning

⬜ D) Help other family members who acknowledge me

Connection with grateful people is medicine. Maybe start small – a lunch, a card, a call to someone who sees you

⬜ E) Donate to causes that matter

You can donate time while saving money. Volunteering might fill some of the caregiving need in ways that don’t bankrupt you

⬜ F) I’d still save it for them somehow

This honesty matters. If you can’t stop giving to them, can you give to yourself too? Even 10% of what you give them?

⬜ G) Other:

Whatever you’d choose reveals what you’re truly sacrificing. Honor that sacrifice by naming it fully

The Government’s Cruel Collection

Parent PLUS loans have special powers. They can:

- Garnish your wages (up to 15%)

- Take your tax refunds

- Reduce your Social Security benefits

- Pursue your estate after death

- Never expire (no statute of limitations)

- Accrue interest during forbearance

You learned this when you tried to negotiate. When you explained your child was estranged, that you were 68, that retirement was impossible. The servicer was sympathetic but clear: “The relationship with your child doesn’t affect your obligation.”

Your obligation. Like love is a contract. Like raising them came with terms and conditions. Like the government is now your child’s enforcement agency, collecting what they won’t acknowledge.

The Other Parents in the Same Boat

You found them online. Forums with names like “Parents of Estranged Children” and “When Love Isn’t Enough.” Thousands of stories. The same story. Different details, same debt.

- Patricia, 71, still paying $890/month, estranged for 7 years

- Robert, 69, declared bankruptcy, loans survived it

- Maria, 73, Social Security garnished, living on $1,100/month

- James, 66, reverse mortgage to pay loans, will die with nothing

- Linda, 70, working at Walmart, child has PhD from Yale

You’re not alone. You’re part of an invisible nation of parents funding their own abandonment. A generation sacrificed on the altar of education costs and cultural change.

The Companies Getting Rich

While you go broke, others profit:

- Navient/Nelnet/Great Lakes: Servicing fees on your suffering

- Universities: Tuition inflated by available loan money

- Therapy practices: Treating the “trauma” you allegedly caused

- Credit card companies: 24% interest on your emotional spending

- Employers: Getting a worker who can’t afford to retire

You’re a profit center for everyone except yourself. A resource extracted until empty. A wallet with a heartbeat.

The Math of Mortality

Your actuarial life expectancy: 14.2 more years (age 82) Loan payoff schedule: 13 more years (age 81) Probability of dying before loan is paid: 46%

You’ve done this calculation at 3 AM more than once. The strange hope that death might be the only discharge. The bitter irony that your funeral might be your final payment.

The life insurance—$500,000 policy—will cover:

- Parent PLUS loans: $67,439

- Second mortgage: $72,000

- Credit cards: $34,822

- Final expenses: $15,000

- Remaining for them: $310,739

They’ll inherit more from your death than you could ever give in life. The ultimate transaction. The final payment. The last deposit into an account that never acknowledges receipt.

What This Is Really About

This isn’t about the money. Except it is. Because money is time. Money is choice. Money is dignity. Money is the ability to say no. Money is the option to rest. And you have none of these.

This is about loving someone more than yourself and paying—literally—for that love.

This is about a system that enables parents to destroy themselves financially for children who can walk away without consequence.

This is about the generation caught between “family is everything” and “cut toxic people out,” paying for both philosophies with compound interest.

This is about dying in debt for someone who might not attend your funeral.

The Terrible Freedom in Truth

Here’s what no one will say: You could stop. Right now. Today. Close the accounts. Cancel the payments. Choose yourself.

Your child has already chosen themselves. They’ve already walked away. They’ve already decided you’re disposable. The only person still choosing them is you.

But here’s what else no one understands: The payments aren’t for them anymore. They’re for you. They’re how you love. They’re how you parent. They’re how you stay connected to someone who severed everything except the financial cord.

The debt is the relationship now. The bills are the bond. The payments are the prayer.

The Line That Lives Rent-Free

Every month when the payment processes, you think the same thing:

“I’m paying $2,144.80 to be someone’s villain.”

It’s the most expensive role you’ve ever played. Method acting where the method is bankruptcy and the audience has left the theater. A performance of love for an empty house.

But here’s the truth that sits deeper than debt:

You’d do it again.

Even knowing how it ends. Even seeing the bills. Even facing bankruptcy. You’d still take out those loans. Still co-sign that lease. Still send that money.

Because love doesn’t learn from consequences. Love doesn’t read terms and conditions. Love doesn’t calculate ROI.

Love just pays.

And pays.

And pays.

Until the account is closed by death or miracle, whichever comes first.

You’re betting on death.

It has better odds.

Frequently Asked Questions – The Debt $ That Doesn’t Die

- Can Parent PLUS loans be forgiven if your child is estranged? No. Parent PLUS loans are legally your responsibility regardless of your relationship with your child. Estrangement, lack of gratitude, or your child’s financial success don’t affect your obligation. The only forgiveness options are death, total permanent disability, or specific employment-based programs. The government will pursue these loans through wage garnishment, tax refund seizure, and even Social Security benefits reduction.

- What happens to Parent PLUS loans when you die? Federal Parent PLUS loans are discharged upon the death of the parent borrower. However, this may trigger a tax bill for your estate (the forgiven amount can be considered taxable income). Private parent loans may not be discharged and could pursue your estate. Always check your specific loan terms.

- Can bankruptcy eliminate Parent PLUS loans? Rarely. Student loans, including Parent PLUS loans, are nearly impossible to discharge in bankruptcy unless you can prove “undue hardship” – an extremely high legal bar. Most parents who declare bankruptcy still keep their Parent PLUS loans. Chapter 13 might help reorganize payments but won’t eliminate the debt.

- How much does the average parent owe in student loans for their children? The average Parent PLUS loan debt is around $30,000, but many parents owe much more. About 3.7 million parents owe collectively over $104 billion. Some parents owe over $100,000. With interest rates at 8.05% and parents often unable to pay down principal, many will die still owing more than they borrowed.

- Should I stop paying for my estranged child’s expenses? This is deeply personal. Financially, continuing to pay for someone who won’t acknowledge you can lead to bankruptcy and destroyed retirement. Emotionally, the payments might be your only connection. Consider setting limits you can afford, seeking financial counseling, and recognizing that love doesn’t require financial self-destruction. There’s no moral obligation to bankrupt yourself for someone who’s cut contact.

End Note: If you’re reading this with a stack of bills beside you, statements for someone who won’t speak to you, know this: Your debt doesn’t diminish your love. Your bankruptcy doesn’t erase your sacrifice. Your financial destruction in service of someone else’s life is still service.

You’re not stupid for paying. You’re not weak for continuing. You’re not wrong for loving past the point of return.

You’re just a parent in a world that’s forgotten what that costs.